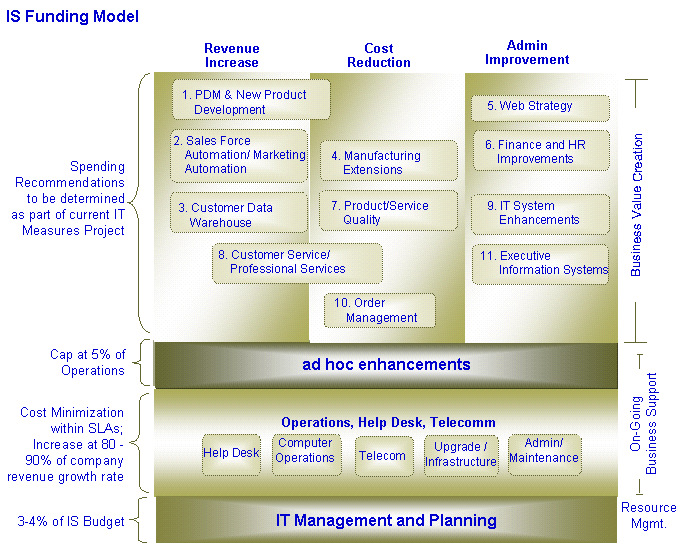

Looking at the model from the bottom up, there is a certain amount of IT

general management, strategy, architecture, planning, etc. that needs to be

done, and benefits the company as a whole. Most well run IS shops keep this to 3

-4% of the overall IT spending. There is really no value in allocating this

back to departments –it is probably best placed directly in the IS budget.

The

second category includes all production activities and costs involved with

providing current services. Best practice is to establish certain service

levels with the business users, then minimize cost to deliver those service

levels. One technique to force this is to keep the rate of increase for

these costs below the overall revenue growth for the company. Exceptions

might be when a major new initiative goes into production. While charging

these costs back to departments helps enlist their support in keeping costs

down, the company may want initially to budget the cost within IS for simplicity.

The

third category, ad hoc enhancements, are small projects (like a new report)

that are requested by a department. These require significant IS management

attention, but do not usually deliver major business value. IS should limit

the total volume of their baseline staff dollars for these requests to 4-6%

of Operations spending, and departments should be required to reallocate

funds from their baseline budgets to pay for the rest of the request. IS

should monitor requests for adherence to the IS architectures.

The top

category is initiatives/projects approved by the IT Steering Committee.

This breaks into three sub-categories: Initiatives to increase revenue;

Initiatives to reduce capital requirements or operating costs; Initiatives

to improve administrative functions (HR, IS, Finance, Legal, etc). Each of

these sub-categories should be capped, but the formula for computing the

caps should be based on the total costs of the initiatives, not just

the IT costs, or people are likely to make sub-optimal decisions on how to

structure projects. The formula for each sub-category will be different (for example,

it might be a straight cap for Admin Improvement; a balance with R&D sales

expenditures for Revenue Growth; and straight ROI up to some limit for Cost

Reduction). There should also be a model capping total expenditures for all

initiatives across all sub-categories. Because expenditures for initiatives

vary widely by quarter, the company will normally take a variable cost approach

(i.e., use contractors) for most of this work, with IS and the business

managing the initiative.

The

team that will do the IT Measures project will provide initial recommended

models and formulae for this category and sub-categories.

For illustrative purposes, the eleven initiatives presented to the IT

Steering Committee in June are mapped by sub-category (note that three

initiatives span sub-categories).