|

Very few business initiatives of any complexity are

100% certain to achieve the objectives set at the price and on the

schedule planned. For IT projects in

particular, there is a substantial body of research that shows that 65% to

70% with budgets of over $1M fail, in the sense of running significantly

over budget or schedule, or failing to deliver a substantial portion of

the promised benefits. About half of the

failures are total failures, where the project gets cancelled or delivers

no value; the other half implements something

but over budget,

over schedule and missing some expected benefits.

The second most common reason for IT

project

failures is lack of adequate organizational change

management (a CEO once made an

astute observation about why his

initiatives had a high success rate: "early on, I conduct public

executions of a few prominent non-supporters, and promote a few

supporters; afterwards the company takes the initiative much more

seriously"). The most common reason for failure, of course, is poor

project or program management.

Companies with a lot of failed and failing

projects, should determine:

-

which projects are in trouble and should

be shut down, and which are worth trying to rescue;

-

which projects appeared to be going along

OK but in fact are risky, and what the quantified risk is; and

-

what the true costs and benefits of

proposed projects are, after adjusting for risk factors.

Risk-adjusted pricing and benefits is a

methodology Kawaru developed (originally for a large technology company)

to allow managers to determine the true cost and potential benefits of a

project. Managers evaluate which success factors are in place at the

particular point in time during a project when they conduct an evaluation

then adjust costs and benefits to reflect the resulting risk score.

There is a quick diagnostic version that a manager can do in a few

minutes, which is based on the premise:

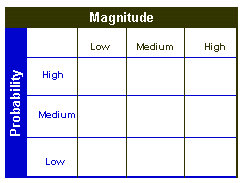

risk comes in two major dimensions:

-

Probability (how likely the adverse event

is)

-

Magnitude (what impact the adverse event will

have).

For example,

building a new high rise in San Francisco, the likelihood of cost overruns

due to planning department and board of supervisors interference is high,

but the magnitude is low to low-medium. The likelihood of a major

earthquake during a vulnerable stage of construction is very low, but the

magnitude is very high.

|

|

Applied to an IT project, this involves the manager going through a

checklist of the major risk factors (program management; resistance to

change; executive sponsorship; size and duration of project; etc.) and

scoring each as low, medium, or high on both dimensions. The manager would

then aggregate the scores (using some judgment; this is not a purely

quantitative process) into a single 3 X 3 matrix. If the low/low box were

checked for the project, that means there is at least a 90% chance that

the project would deliver most of the projected benefits close to on time

and budget. If high/high, stop wasting your money. If you view the lower

left box as "lo w/low,"

then, in most situations, checks in the three boxes to the lower left mean

'go,' in the three on the upper

right mean 'stop;' and the diagonal from the upper left to lower right

means 'find ways to mitigate risk before proceeding. w/low,"

then, in most situations, checks in the three boxes to the lower left mean

'go,' in the three on the upper

right mean 'stop;' and the diagonal from the upper left to lower right

means 'find ways to mitigate risk before proceeding.

This proves more useful when a manager completes two matrices: one for

project cost/schedule; and one for project

benefits. With enough data points, a company might find that for it a

check in the middle box of the benefits matrix means there is a 60% risk

factor to the benefits (the project would, statistically speaking, deliver

only 40% of the projected benefits). This means that the cost per dollar

of benefits is really 2.5 times as much as the notional original analysis

indicated. If a project is expected to cost $5M and deliver $25M in

benefits, or 5:1, but the middle box was checked, then risk adjusted

benefits are really only $10M, or 2:1. If a company invests an additional

$1M getting the risk factor down to 40%, then risk adjusted benefits

increased to $15M, or 2.5:1 overall and 5.0.1 incrementally ― a good investment. Apply similar logic on the

project cost/schedule side: calculate the risk in the schedule and budget

estimates, then adjust cost/schedule to reflect the risks, and recalculate

the cost/benefit ratio.

While specific cost/schedule and benefit risk

percentages vary company to company, the methodology can be used in a more

qualitative way to achieve similar result. Basically, if an evaluation of

the current situation puts the project in the middle square of the matrix

for cost/schedule, and the company can lower it to one of the bottom left

three boxes for another $xx,xxx, then clearly that would be a good thing

to do. If a company can also reduce the risk on the benefits side for a

fairly small $$$ investment, that would be even better. Doing both would

be excellent. However, continuing to evaluate project decisions as if there is no

risk to either project cost and schedule or to project benefits from the

decision could be disastrous.

|