Initial

Position

Given all

that has been stated above regarding Global 5000 companies’ ability to

transform, we posit several reasons that they have not been able to

transform thus far. First and foremost, lack of senior executive support

of transformative initiatives, which almost always involves technology, is

a major barrier to success. If the Internet is considered as a proxy for

pervasive, real time information availability along the value chain, then

this finding explains some of the lack of enthusiasm on the part of CEOs

to invest heavily of their own time and their company’s resources in

transformation initiatives.

Secondly,

each region, Western Europe and Asia Pacific, face different barriers

based on where they are in terms of technological infrastructure,

governmental infrastructure (independent institutions for corporate

governance, etc.) and policy, and financial institutions and

infrastructure.

North

America is substantially ahead, not just chronologically but structurally

(government, unions, capital markets, corporate governance, competitive

nature of economy). Europe today is focused on improving infrastructure,

when what they require is improved governance structures. Implication:

Europe is not 2 years behind North America – it is structurally impaired

versus North American and will not be able to leverage information

abundance as well.

Asia

Pacific is not a single entity, as each country is remarkably different

from the other in its current position. On the whole, these counties are

more behind than Europe, but more willing to adopt unconventional

approaches to catch up (Japan), invest heavily in infrastructure (Korea,

Singapore) or accept secondary roles (for now) in transformed value chains

(Greater China).

Much has

been made of the infrastructure advances in wireless (Europe and Japan),

broadband (Korea), and pervasive access (Singapore). These claims confuse

transport with product, as described in Finding 3.

Findings

1)

Established companies are organized and governed to accomplish incremental

business model changes, not disruptive changes. Only long-term persistent

CEO leadership has the potential to drive the necessary company and value

chain transformation required to leverage information abundance.

In East Asia, for many counties, the government has considerable

influence over the business and is tied in through various investments,

etc. In China, many of the industrial corporations are State Owned

Enterprises (SOE), which typically consume more capital than they are

able to produce, accounting for 80% of the countries bank loans. Within

the SOE’s there are often layers of subsidiaries underneath, run by

elites who typically pay themselves for dubious services, then report

losses to the holding company (1). These families dominate the SOE’s and

are not held accountable to anyone, as there is not an independent

corporate agency to act as an adversary. It is difficult to lead a

company through a transformation when the leaders are not the people

with power and those with power are not incented to change.

Leadership style to transform the value chain is a major factor in

success or failure of the initiative. Key attributes for a leader

undertaking this type of initiative is:

·

Willingness to make decisions with very little information

·

Knowledge of human motivation, proper incentive programs in place, provide

your best people with authority and autonomy

·

Radiate and support a vision

·

Goal focused versus process focused

The small percentage of companies that have successfully transformed,

have all had the executive support and drive to take them there.

‘Greenfield’ companies do not face this obstacle, but often do not have

the leverage that comes with ownership of the brand to transform their

value chain.

For companies based in France, where the country is heavily

bureaucratic, highly-centralized and run from the top down, it is next

to impossible to create the type of environment, such as Charles

Schwab’s, where leadership is instilled within employees at all levels

of the company.

Leadership in Germany is also difficult because of the dilution of CEO

power due to:

·

Union involvement on supervisory board;

·

German government involvement on the state and federal level;

·

And a cultural tradition that mitigates against high profile executives.

2)

A small

percentage (1-2%) of the Global 5000 have actually accomplished or are

well along towards accomplishing value chain transformation utilizing

information abundance as an enabler.

Companies whose products incorporate substantial technology, and whose

products are heavily used by the high tech and telecommunications

industries, are heavily represented among the success stories. Several

information intensive industries (e. g., health care delivery;

insurance) have essentially no major successes. What successes exist are

largely North American based.

Furthermore, in Europe, companies based in the U.K., France, and Germany

have more trouble implementing pan-European strategies because of

traditional national prejudices/animosities by many countries towards

these three. Companies that have the capital structure and mass to

transform industries/value chain pan-European are predominately in UK,

France and Germany. Therefore, the pan-European value chain

transformation is hindered by the lack of adequately capitalized players

without historical baggage.

For those companies based in European counties, capital will be sparsely

allocated to non-traditional players, and most investors will only fund

start-ups that have a detailed, long-term strategy in place. In

comparison, many North American investors fund start-ups without

long-term plans that have the management teams in place that have the

ability to react to disruptive change and make quick decisions to move

forward.

3)

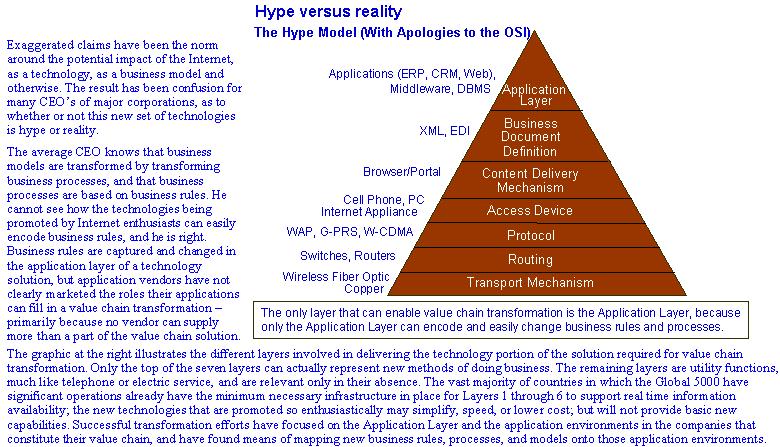

Almost

two thirds of CEO's consider the business change potential of "the Web" to

be more hype than reality, due in part to exaggerated and unrealistic

claims by proponents. Many CEOs (and other Cxx officers) do not

distinguish between the technology enablers (the Internet; XML;

middleware) and the outcome (abundant, complete, pervasive, real time

information availability across a value chain).

Given the success stories that exist for value chain transformation in a

variety of industries, this skepticism on the part of two thirds of CEOs

might appear puzzling. Further discussions have shed some light,

however, on the caution with which senior executives to the assertions

of the proponents of the change potential of the Internet. Three factors

appear to elicit the negative executive reaction:

·

The focus

on technologies on the part of proponents:

4

Wireless

technologies, such as cell phones, wireless protocols (WAP, GSM, GPRS, W-CDMA,

3G wireless), Internet appliances

4

Backbone

technologies, such as fiber optics, switches, routers

4

New

Internet conventions and tools, like XML and others too numerous to

mention. As much of this hype is promoted by vendors selling products, the

focus on technologies is understandable, but the average CEO has had

enough “silver bullet” technologies fail to deliver promised benefits

(think client/server or ERP) to be rightly resistant to such claims.

·

The lack

of any plausible causal explanation of how the hyped technologies tie to

what the CEO knows are the critical success factors of his business – how

does an Internet-enabled cell phone in the hands of every Scandinavian

reduce his company’ working capital requirements? Improve gross margins?

Speed time to market?

·

The sheer

messianic intensity of many of the proponents appears to most executives

more appropriate to a new religious cult than to a business setting.

4)

USA and

Canadian companies are disproportionately represented among

global players leveraging information abundance.

Not

only have virtually no European or East Asian headquartered companies

achieved the value chain transformation; but the number of such

companies currently attempting transformation, even in their home

geographies, is less than the North American-based companies with

initiatives in those geographies. The one exception appears to be some

Taiwanese manufacturers, but they may be driven by requirements of their

U.S.-based customers.

In both

Western Europe and Asia Pacific, the culture that pervades is one that

does not celebrate success and punishes failure, discouraging executives

from high risk, high reward initiatives. In North America, particularly

the U.S., failing in a job and reinventing one’s self is part of the

culture; in both Europe and Asia Pacific, it is inconceivable. Stock

options are used in North America to provide rewards commensurate with

risk and motivate employees, but in Western Europe, stock options are

less practical because the laws and customary practice are not

supportive. Europeans view their family, vacation time, and regular work

hours as a high priority and thus far have not developed the culture and

enablers compelling enough to move them from their secure high paying

jobs, to opportunities with high risk and potentially little reward. A

value chain transformation is inherently disruptive, requiring that

management and employees are properly incented to execute the change.

5)

The

owners of the brand and of product/service design have the

greatest leverage in transforming the value chain and extracting

disproportionate profit.

Manufacturing and financing/capital provision no longer generate above

average margins, except during capacity constrained periods in a

business cycle. Companies interested in maintaining consistently high

margins and return on capital (which tend to be more important

motivators for U.S.-based companies) are increasingly using third

parties to perform activities that have lower margins or employ more

capital, as a way of overcoming internal barriers and resistance to

value chain transformation.

Several country-specific strategies in East Asia today:

4

Japan continues to stay strong in branding and design while leveraging

North American firms to help with the transformation.

4

Greater China has temporarily accepted secondary role in the value chain

transformation and will participate if driven by external factors, such as

North American customers and foreign investors.

4

Korea is still following Build-to-Order manufacturing, running as

autarchic companies and focusing on infrastructure rather than the

customer.

4

Australia is relatively comfortable with where they are as a raw materials

supplier except for a few leading companies, such as BHP.

View the

Broken Hill Proprietary

Transformation Initiative

6)

Certain

companies and cultures are attempting to partner with firms that have

accomplished a value chain transformation, to obtain a kick-start or

“piggyback effect:” DoCoMo with AOL; NEC with Cisco; Mitsubishi with

Inktomi and others.

East Asia is looking to the United States to serve as a hub to Internet

technology and IT that will transform their value chains and bring them

up to speed through partnerships. A recent example of such partnerships

occurred in September of 2000, between Japanese company NTT DoCoMo and

U.S.-based AOL, to jointly develop and market mobile-Internet services

in Japan and elsewhere. AOL Japan, Inc. will be the center point for

future investments and innovative Internet mobile services, owned and

controlled mostly by parent company, AOL and NTT DoCoMo.

The Cisco-NEC relationship aims to expand globally expand the

collaboration the two companies have historically demonstrated at a

regional level. In Japan, NEC has a broad OEM arrangement with Cisco,

providing joint solutions to the market. In the United States, NEC is

one of the largest system integrators for Cisco; and in Australia, NEC

and Cisco operate under a joint marketing agreement.

Inktomi and Mitsubishi have formed a partnership to bring Internet

infrastructure into Japanese companies. As spoken by Koichi Kobayashi,

corporate vice president, from Mitsubishi Electric Corp, "believe

Inktomi's cache technology and portal products and services are keys

ingredients for the next generation Internet and we expect to launch

Traffic One Communications, our new Internet business subsidiary in

early October to leverage these technologies,"

7)

Implicit

knowledge especially in conjunction with lifetime employment is a barrier

to value chain transformation. Explicit knowledge in highly mobile labor

forces is an enabler.

How

does a company undertake a value chain transformation if it operates

using the implicit knowledge in the heads of its employees, rather than

explicit documentation? The answer is, it doesn’t. A company that

operates under implicit knowledge relies on handshakes for contractual

agreements, as many of the companies within the Chinese guaxni networks

do, rather than a legal-binding document with terms of agreement. Most

East Asian companies and institutions operate through implicit knowledge

rather than explicit: witness China’s most recent reaction, as described

by The Economist, to the rules for entering the WTO, where the “Chinese

argue that no member should be subject to more than the WTO’s existing

rules, and insist that “mutual trust” and “mutual confidence” ought to

be enough.”

How

easy is it for a company to then break a contract with one of its

suppliers or vendors to re-orientate itself in the value chain based on

new initiatives? It cannot. Furthermore, employees with the implicit

knowledge are operating under the assumption that they will perform that

particular job for an extended period of time and there is very little

mobility. All of the knowledge that the single employee has gained is

kept within his/her own mind, making it difficult to shift, replace or

add new employees to fill that role.

“It is difficult bordering

on impossible to lead a company through transformation when leaders are

not the people with power, and those with power are not incented to

change.

Corporate governance

structures in Northern Europe, Japan and mainland China prevent the

required accumulation of power at the CEO level to drive value chain

transformation.”

8)

Most

ecosystems in North America have at least one value chain dominated by a

company able to transform the value chain. This is typically the company

with the brand or design presence and the initiative to undertake the

transformation.

This

suggests that North America will produce most of the global leaders in

the new ecosystems that are supplanting traditional industry boundaries.

When an ecosystem leader fails to seize leadership, the second or third

place company can step in.

The

element present in most North American based ecosystems, and incomplete

elsewhere, are a variety of specialized firms focused on performing only

one or a small number of activities within a value chain, but performing

these activities for many value chains across an ecosystem.

Incorporating these firms into a value chain permits the owner of the

brand/design greater flexibility, dramatically reduces the capital

required to operate, and encourages management to focus on the highest

customer value add activities. Within North America, only a few

regulated or formerly regulated industries/ecosystems (such as

traditional telephone operating companies) have the full range of

specialty firms but lack any branded player willing to lead value chain

transformation.

9)

Each

region has specific barriers:

Asia

Pacific:

·

Lack of

information transparency (will change to please foreign investors)

·

Lack of

accepted corporate governance standards and accountability

·

Government influence on financial sector and capital allocation

·

Lack of

an “Asian” business model (Japan, China and Taiwan, etc. All have their

own models)

·

Government regulation protects status quo and discourages innovation

4

Example: NTT

4

Competition Policy favors established companies (chaebol in Korea,

kieretsu in Japan, etc.) Exceptions: Taiwan and Hong Kong (pre-China

return)

·

Family

dominated businesses rely on implicit knowledge and have thin management

teams. Relationships with other firms rely heavily on “guanxi” which is

hard to computerize

·

Most

Asian cultures do not support high profile success and condemn failure

Europe:

·

Government emphasis on information management leads to regulations that:

4

Discourages business from sharing information;

4

Creates

high compliance costs;

4

Insists

government access to company information; and

4

Causes

a reluctance to establish operations in these counties.

·

Existing stakeholders who will be adversely impacted by change (unions,

alliance partners, regulators, mgmt) have power to block change.

·

Failure

is punished more than success is rewarded.

·

Upside

for top management is limited – reduces willingness to take risks

·

Capital

sourcing practices have created cross holdings and grouping of business

around the capital provider on the Continent. This makes structuring

value chains that cross groups harder than value chains within

groups, even when the former is more effective.