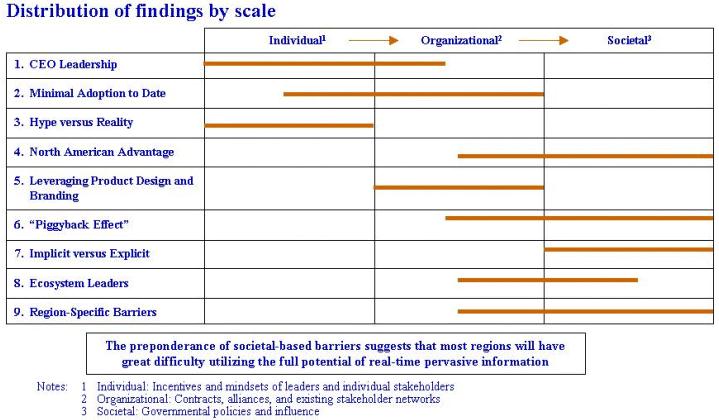

1.

Established

companies are organized and governed to accomplish incremental business

model changes, not disruptive changes. Only long-term persistent CEO

involvement has the potential to drive the necessary company and value

chain transformation required to leverage information abundance.

2.

A small percentage (1-2%) of the Global 5000 have actually

accomplished or are well along towards accomplishing value chain

transformation utilizing information abundance as an enabler. Companies

whose products incorporate substantial technology, and whose products are

heavily used by the high tech and telecommunications industries, are

heavily represented among the success stories

3.

Almost two thirds of CEO's consider the business change potential

of "the Web" to be more hype than reality, due in part to exaggerated and

unrealistic claims by proponents. Many CEOs (and other Cxx officers) do

not distinguish between the technology enablers (the Internet; XML;

middleware) and the outcome (abundant, complete, pervasive, real time

information availability across a value chain).

4.

The owners of the brand and of product/service design have the

greatest leverage in transforming the value chain (and extracting

disproportionate profit). Manufacturing and financing/capital provision no

longer generate above average margins, except during capacity constrained

periods in a business cycle.

5.

Certain companies and cultures are attempting to partner with firms

that have accomplished a value chain transformation, to obtain a

kick-start or “piggyback effect:” DoCoMo with AOL; NEC with Cisco;

Mitsubishi with Inktomi and others.

6.

Reliance on implicit knowledge in the workforce, especially in

combination with lifetime or extended tenure employment, is a barrier to

value chain transformation. Explicit knowledge in a highly mobile labor

force serves as an enabler.

7.

Most ecosystems in North America have at least one value chain

dominated by a company able to transform that value chain. This is

typically the company with the brand or design presence, and the CEO

initiative to undertake the transformation.

8.

There are some disablers that are unique by major geography:

Europe:

·

Government emphasis on information management leads to regulations that:

discourage business from sharing information; high compliance costs,

insistence on government access to company information, and reluctance

to establish operations in these counties

·

Existing stakeholders who will be adversely impacted by change (unions,

alliance partners, regulators, management) have power to block change.

·

Failure is punished more than success is rewarded

·

Upside for top management is limited – reduces willingness to take risks

Asia

Pacific:

·

Lack

of information transparency (gradually changing to meet foreign

investors’ demands)

·

Lack

of accepted corporate governance standards and accountability

·

Government influence on financial sector and capital allocation

·

Lack

of an “Asian” business model (Japan, China and Taiwan, Korea, etc., all

have their own models)

·

Government regulation protects status quo and discourages innovation

·

Family dominated businesses rely on implicit knowledge and have thin

management teams. Relationships with other firms rely heavily on

“guanxi” which is hard to computerize

·

Most

Asian cultures do not support high profile success and condemn failure